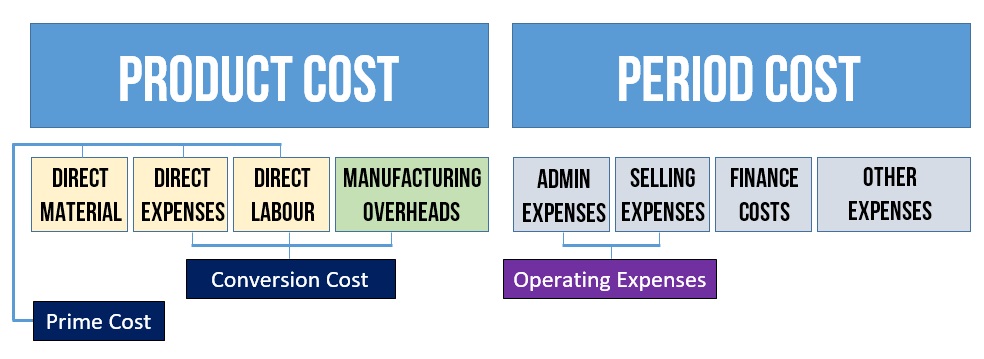

Product costs or Inventoriable costs are all such costs that form part of the inventory.These are basically such costs that relates directly to the products and are incurred to produce such products and also include the costs that are incurred to bring these products into saleable condition (or simply present location and condition).

Product cost include:

direct material costs

direct labour costs

manufacturing overheads

any other cost incurred specifically for example:

carriage inwards, royalties or any other direct expense

handling and storage costs; if they are part of the production process and it cannot be completed without storage for some time. For example fruit (to ripen), pickles etc.

1.1 Direct material cost

Direct materials are such materials that are directly associated with cost object and their cost can be traced back to cost object i.e. product or cost center with reasonable accuracy and certainty.

These are usually raw materials that are converted to finished inventory but does include other material if their cost can be traced. For example, cloth in furniture etc.

Materials like oil, nails or screws are hard to be account for and thus their cost cannot be traced to cost object easily and therefore treated as indirect material. Indirect material are considered manufacturing overheads.

1.2 Direct labour cost

Direct labour are the workers that are involved in production process i.e. actually converting the goods from raw material to work in process or finished goods. The cost of such labour is treated as direct labour cost. Technically direct labour cost is the cost that can be associated to particular product or cost object and its cost be traced back easily. For example, labour working on product AAA or particular assembly line.

Personnel like production supervisors, although they are present at factory floor instructing workers, are not considered direct labour and are called indirect labour and treated as manufacturing overheads. Main reason for doing so is that cost associated to such personnel is difficult to ascertain in relation to particular cost object.

For example a production supervisor that is responsible for instructing labour working on three different products, it is difficult to divide the supervision cost among three products. What basis should we use to divide the cost? Time? Number of instructions? Units produced? There is no clear way to do it.

It is important to note that personnel outside production activity e.g. administration or sales staff are accounted for neither as direct labour nor manufacturing overheads. They are treated as non-manufacturing overheads.

1.3 Manufacturing overheads

Manufacturing overheads or simple overheads are all such costs other than direct material cost, direct labour cost and any other directly expenses. Technically manufacturing overheads include all such costs that were incurred as part of production but cannot be associated directly to specific cost object (product) or their cost cannot be traced easily. Thus treated as manufacturing overheads.

In other words manufacturing overheads is like a reserve where production cost are “binned” if they escape direct material, direct labour costs or direct expenses. For example, factory rent, depreciation of machinery, heating and lighting costs, repairs etc.

2 Period Cost

Period costs or non-inventoriable costs or non-manufacturing overheads are all such costs that are not incurred in connection to the production. Rather they are connected and measured in context of time. These costs do not play any role in producing the asset or bringing the asset to its present location and condition. These are basically such costs that are non-manufacturing in nature and thus do not form part of inventory cost.

According to CIMA Official Terminology, period cost is:

Cost relating to a time period rather than to the output of products and services

These are called period costs because they are reported in the period in which they are incurred and cannot be carried forward to the next period as opposed to the product costs which are absorbed in the products and are reported in the period in which they are sold.

Examples of these costs include:

administrative costs

selling and marketing costs

finance costs or borrowing costs (excluding such costs that can be included in the inventory), product research costs

product development costs that failed to fulfill capitalization criteria

abnormal losses etc.

3 Impact of choice of costing techniques

Another important fact to consider is that how costs are to be classified and treated also depends on the type of accounting being used i.e. financial accounting or cost and management accounting and costing techniques used.

For example under absorption costing all the manufacturing costs whether variable or fixed, direct or indirect are treated as product costs. Whereas under marginal costing technique, only variable manufacturing costs are treated as product costs and fixed production overheads are treated as period costs.

Going bit deeper in costing techniques and cost accounting techniques, we see under Throughput accounting all production costs except direct material costs are treated as period costs like direct labour etc is also treated as period cost. Whereas under Life Cycle costing all the costs incurred right from the beginning i.e. research and development until the product is disposed or consumed are considered as part of the inventory i.e. product cost.

In short, things are simple if they are kept simple for example under financial accounting the distinction between these two is easy thanks to accounting standards. However, under cost and management accounting with new costing and management techniques the classification of different costs is not static or standardised and one cost may be taken as product cost under one costing and management model and the same cost may be taken as period cost in the other model.

4 Charging product cost of goods sold to the period

Though its a little too early to discuss and we will return to this aspect in more detail under cost accounting records topic, but product cost of units sold during the period is also considered period cost once units are sold to customers and are charged to income statement whereas, product cost of units not sold during the period is recorded as closing inventory in balance sheet.

So the above diagram can be extended as following:

But don’t worry if its too overwhelming or causing confusion for now as we will be discussing it more detail in later lessons.